Ssae 18 Control Objectives List

The Astounding Ssae 16 Audit Soc 1 Soc 2 Soc 3 From Lazarus Alliance With Regard To Ssae 16 Report In 2020 Best Templates Professional Templates Business Template

The New Us Assurance Standard Ssae 18 Compact

The Clarity Project Ssae 18 Essentials

Https Guidehouse Com Media Www Pdfs Legacy Guidehouse Whitepapers What Are Ssae No 18s And How Pdf

Soc 1 Vs Soc 2 What S The Difference Wipfli

Preparing For A Soc Audit A Checklist

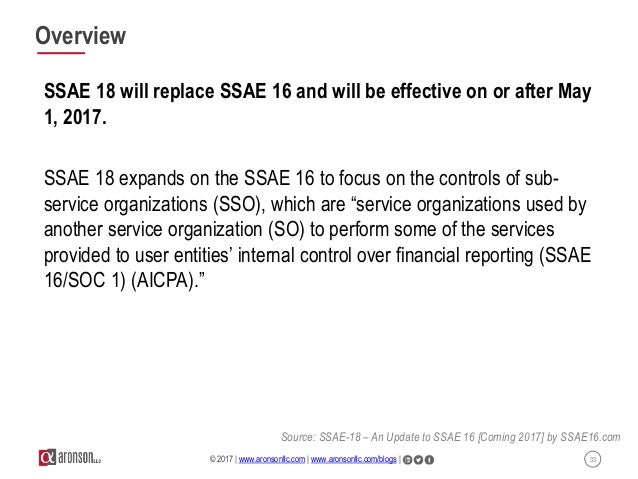

Moving to ssae 18.

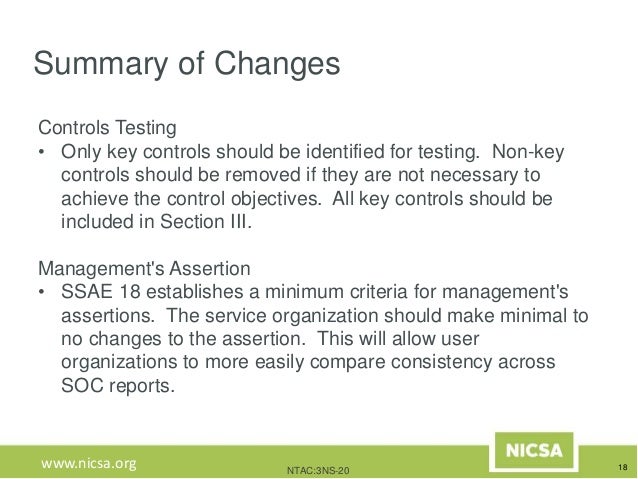

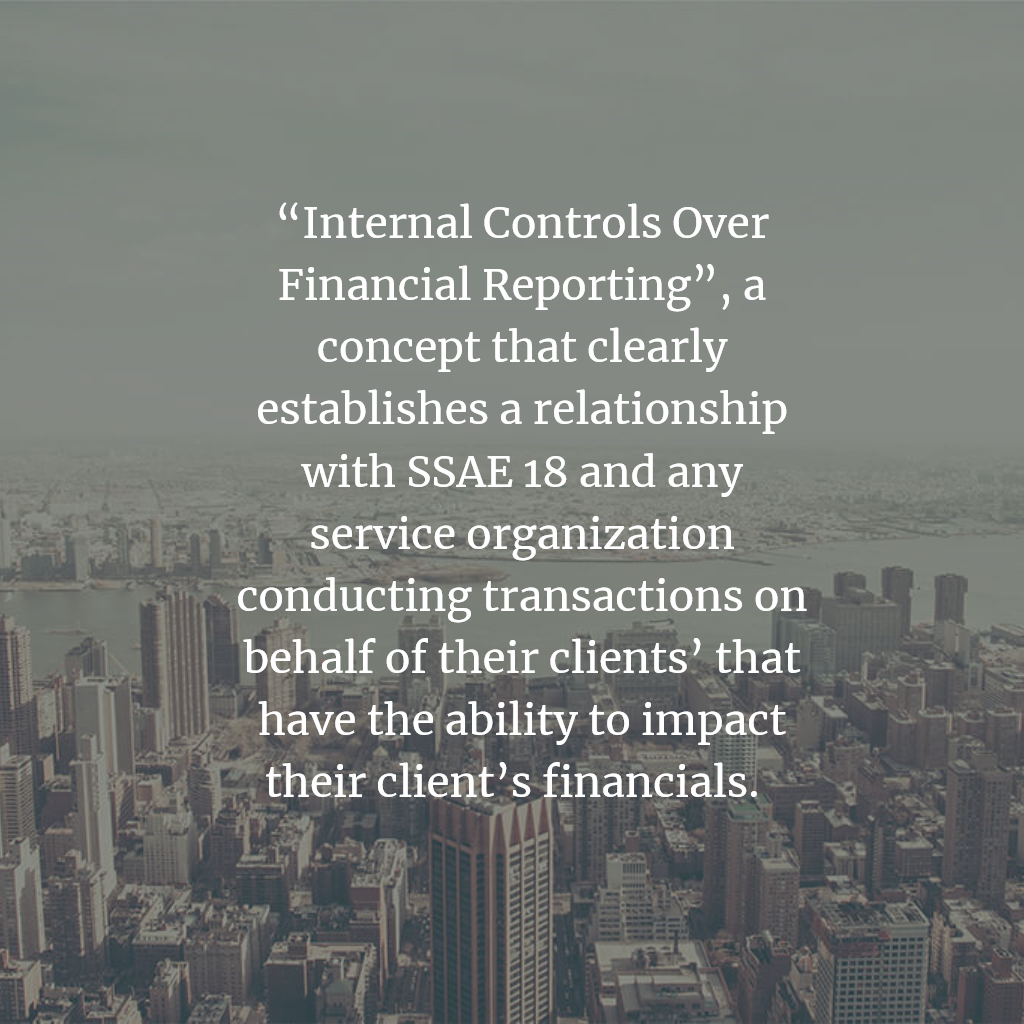

Ssae 18 control objectives list. Control objectives address the risks that controls are intended to mitigate. Are necessary to achieve the control objectives stated in management s description of the system when the carve out method of reporting has been used. A clearer view of attestation standards for service organizations 1. The aicpa s control objective definition provided in ssae 18 is the aim or purpose of specified controls at the service organization.

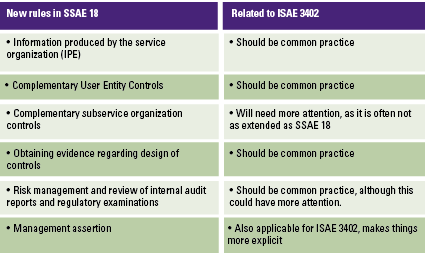

Changes for service organizations themselves revision what service organizations need to do differently csocs a complementary subservice organization control csoc is a control that management assumes will be implemented by their subservice organization. Since ssae 18 has effectively replaced ssae 16 and also sas 70 and because the ssae 18 controls and related assertions need to be based on relevant internal control over financial reporting icfr service organizations need to constructively re think their control objectives. Focuses on the impact of ssae 18 on soc 1 examinations and the re codified attestation standards specifically at c section 105 and at c section. Developing soc 1 ssae 18 control objectives that are related to the icfr concept is critical.

Ssae 18 Soc Audit And Attestation Services Riskpro India Connect With Risk Professionals

Business Trip Report Template Pdf 3 In 2020 Report Writing Template Sales Report Template Report Writing

Ssae 18 Soc 2 Certified Lifeline Data Centers

Control Objectives Activities What Are They What S Appropriate

Soc 1 Ssae 18 Audit Checklist For Auditing Success For Denver Co Businesses Ndb Accountants

Introduction To Ssae 18 And Service Organization Controls Soc Examinations Mckonly Asbury

Soc For Service Organizations Information For Cpas

Ssae 18 The Full Overview For Vendor Management

Webinar Soc Reports 101 Boost Your Business Bottom Line

Soc And Ssae Reporting Services Coalfire

Https Www Giac Org Paper Gsna 553 Understanding Service Organizations Ssae 111066

What Is Soc 1 Ssae 18 Introduction And Overview

Soc 1 Type 2 Compliance Audit Ssae 18 Vs Soc 1 Faq Isae 3402 Icfr Sox Auditor

Health And Safety Incident Report Form Template 9 Templates Example Templates Example In 2020 Health And Safety Incident Report Report Template

What Is A Soc 1 Report Soc 1 Videos Kirkpatrickprice

2020 Trust Services Criteria Principles For Soc 2 Tsp Section 100

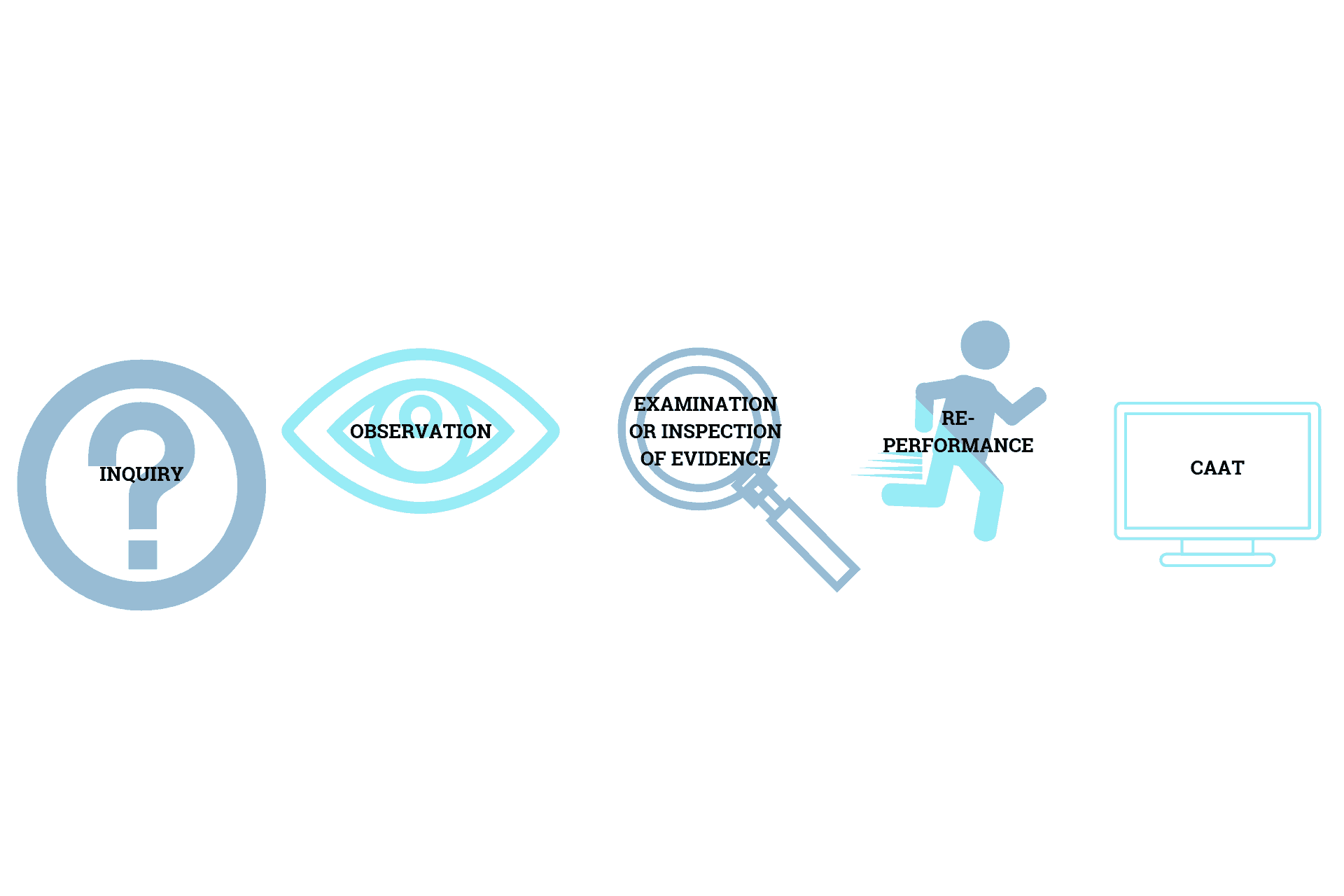

5 Types Of Testing Methods Used During Audit Procedures I S Partners

Https Www Dcma Mil Portals 31 Documents Policy Dcma Man 4301 11v2 Pdf Ver 2019 10 02 110921 410

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsickyqjeazia57ci0f4m Y6y7cnzyszorcrmv La07y93xw13k Usqp Cau

Soc 1 Vs Soc 2 Reports Difference Between Determining Needs

Wk6gzehrjrdgm

Subservice Organizations Carve Out Audit Vs Inclusive Audit Methods

Soc 2 Compliance Audit Checklist 2020 Know Before Audit

What Is A Soc 1 Report When Is It Required Who Needs It

Soc 2 Vs Nist 800 53 What You Need To Know

Caine Weiner Achieves Ssae 18 Status Kam

Moving To Ssae 18 What Has Changed For Soc Reports Brown Smith Wallace

Research Report Sample Template 6 Templates Example Templates Example Research Paper Outline Research Paper Paper Outline

Cloud Archives All Covered

Health And Safety Incident Report Form Template 9 Templates Example Templates Example In 2020 Health And Safety Incident Report Report Template

What Is An Assertion Audit Management Financial Soc Reports

Https Www State Wv Us Admin Purchase Bids Fy2018 B 0705 Lot1800000001 01 Pdf

Https Chapters Theiia Org San Diego Documents Presentations Kpmg Soc 20training 20and 20ssae 2018 20overview Iia 20presentation V2 Pdf

Https Arc Fiscal Treasury Gov Files Pdf Arcssae8soc1reportasof06 30 19 Oig 19 043 Pdf

Cobit 2019 Audit Checklist Reciprocity

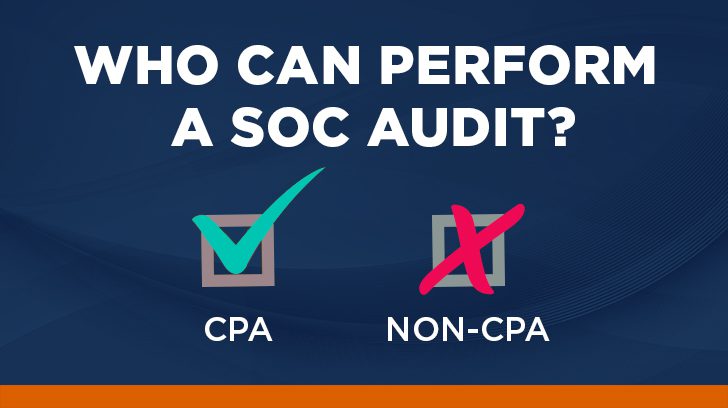

Who Can Perform A Soc Audit Cpa Non Cpa Soc 1 Soc 2

8 Tips For Understanding Attestation Engagements Under Ssae 18 Cpa Practice Advisor

Ssae Soc Audits Auditee Auditor Assessor Virtual Event Tickets Mon Aug 31 2020 At 8 45 Am Eventbrite

What Is Ssae 16 Definition From Whatis Com

What Is A Soc Report Do You Need One Moore Colson Primeglobal

Ssae 18 Carve Out Vs Inclusive Method I S Partners Llc

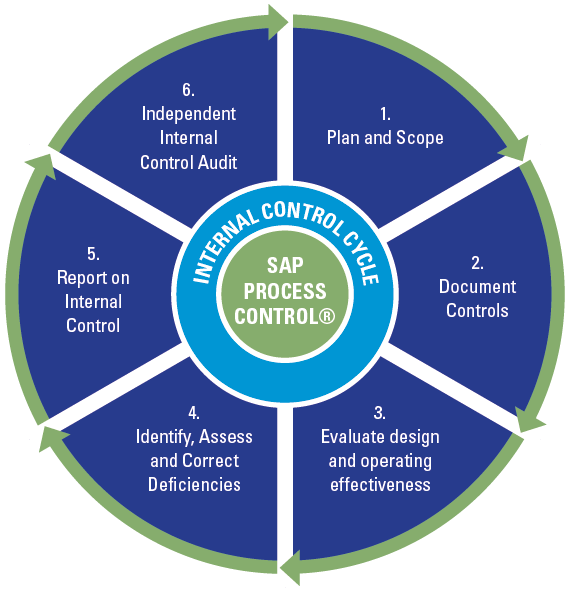

A Practical View On Sap Process Control Compact