Ssae 18 Controls List

The Astounding Ssae 16 Audit Soc 1 Soc 2 Soc 3 From Lazarus Alliance With Regard To Ssae 16 Report In 2020 Best Templates Professional Templates Business Template

Ssae 16 Report Template 11 Templates Example Templates Example In 2020 Report Template Templates Professional Templates

Ssae 16 Report Template 12 Templates Example Templates Example In 2020 Report Template Templates Professional Templates

What Is Ssae 18 Certification

The New Us Assurance Standard Ssae 18 Compact

Cloud Security Management Policy Monitoring Cloud Security Solutions Security Solutions Data Integrity Security Tools

Another series we will have periodic posts about will be related to potential controls that would be expected to be in place almost regardless of the entity in question.

Ssae 18 controls list. The ssae 18 reporting standard soc 1 soc 2 soc 3 formerly ssae 16 support and guidance for ssae18 soc 1 soc 2 and soc 3 reporting standards formerly ssae 16. Clarification and recodification which seeks to clarify the requirements and provide application guidance for performing and reporting on examinations reviews and agreed upon procedure engagements attestation engagements. A soc 1 type 1 report is an independent snapshot of the organization s control landscape on a given day. The changes made to the standard this time around will require companies to take more control and ownership of their own internal controls around the.

18 redrafts all ssaes with the exception of ssae no. Clarification and recodification supersedes statement on standards for attestation engagements nos. Developing soc 1 ssae 18 control objectives that are related to the icfr concept is critical. A soc 1 type 2 report adds a historical element showing how controls were managed over time.

Statement on standards for attestation engagements no. 15 an examination of an. Standards for 18 attestation engagements issued by the auditing standards board attestation standards. Ssae 16 mirrors the international standard on assurance engagements isae 3402.

Ssae 18 tуре ii соmрlіаnсе controls include facilities аnd аѕѕеt mаnаgеmеnt logical ассеѕѕ аnd access control network аnd іnfоrmаtіоn ѕесurіtу соmрutеr ореrаtіоnѕ bасkuр аnd recovery сhаngе аnd іnсіdеnt mаnаgеmеnt organizational аnd аdmіnіѕtrаtіvе соntrоlѕ. 15 guidance moved to au c section 940 with the issuance of statement on auditing standards no. Auditing standards board issued ssae no. Ssae 18 is a series of enhancements aimed to increase the usefulness and quality of soc reports now superseding ssae 16 and obviously the relic of audit reports sas 70.

This document focuses on the impact of ssae 18 on. The aicpa s control objective definition provided in ssae 18 is the aim or purpose of specified controls at the service organization. The most significant changes in ssae 18 may slightly impact service organizations with the addition of new controls and report enhancements but it will have the benefit of providing additional assurance to user organizations. Since ssae 18 has effectively replaced ssae 16 and also sas 70 and because the ssae 18 controls and related assertions need to be based on relevant internal control over financial reporting icfr service organizations need to constructively re think their control objectives.

Well the authoritative source for a soc 1 audit is the american institute of certified public accountants statement on standards for attestation engagements number 18.

Business Trip Report Template Pdf 3 In 2020 Report Writing Template Sales Report Template Report Writing

Replicon Ssae 18 Compliance Audit Checklist

Https Guidehouse Com Media Www Pdfs Legacy Guidehouse Whitepapers What Are Ssae No 18s And How Pdf

The Ssae 16 Reporting Standard Soc 1 Soc 2 Soc 3 Managed It Services Certified Public Accountant Standard

Health And Safety Incident Report Form Template 9 Templates Example Templates Example In 2020 Health And Safety Incident Report Report Template

Portfolio Management Reporting Templates 1 Templates Example Templates Example In 2020 Senior Management Portfolio Management Templates

Ssae 18 Compliance Nexcess

Soc 1 Ssae 18 Checklist

Research Report Sample Template 6 Templates Example Templates Example Research Paper Outline Research Paper Paper Outline

Portfolio Management Reporting Templates 4 Templates Example Templates Example In 2020 Professional Templates Portfolio Management Report Template

How Ssae 18 Will Impact Soc 1 Reports

Hipaa Compliance Ssae 18 Key Information Systems

Ssae 18 Soc 2 Certified Lifeline Data Centers

How To Write A Work Report Template 6 Professional Templates In 2020 Report Template Evaluation Templates

Test Closure Report Template 5 Templates Example Templates Example Report Template Templates Professional Templates

Ceo Report To Board Of Directors Template 1 Templates Example Templates Example In 2020 Board Of Directors Director Ceo

Research Project Report Template 1 Templates Example Templates Example In 2020 Research Projects Report Template Report Writing Template

Health Check Report Template 5 Professional Templates In 2020 Health Check Report Template Templates

1

Accident Report Form Template Uk 1 Professional Templates Incident Report Report Template Incident Report Form

L D Report Template 4 Templates Example In 2020 Report Template Professional Templates Templates

Daily Work Report Template 2 Gagasan Blog

What Is Soc 1 Ssae 18 Introduction And Overview

Section 7 Report Template 1 Templates Example Templates Example In 2020 Report Template Professional Templates Statement Template

Sales Call Reports Templates Free 5 Templates Example Templates Example In 2020 Report Template Templates Templates Free Download

Football Scouting Report Template 6 Templates Example Templates Example Report Template Templates Professional Templates

Failure Analysis Report Template 4 Templates Example Templates Example In 2020 Report Template Templates Analysis

Health And Safety Incident Report Form Template 9 Templates Example Templates Example In 2020 Health And Safety Incident Report Report Template

Real Estate Report Template 4 Templates Example Templates Example Report Template Templates Real Estate Templates

Cwe Common Weakness Enumeration Vulnerability Cool Tech Checklist

Image Result For Criminal Case Files First Letter Documentation Examples Report Writing Template Report Writing Format Report Template

Health Check Report Template 5 Professional Templates In 2020 Health Check Report Template Templates

Threat Assessment Report Template 6 Professional Templates Classroom Newsletter Template Report Template Assessment

Caine Weiner Achieves Ssae 18 Status Kam

Conference Report Template 7 Professional Templates Report Template Templates Professional Templates

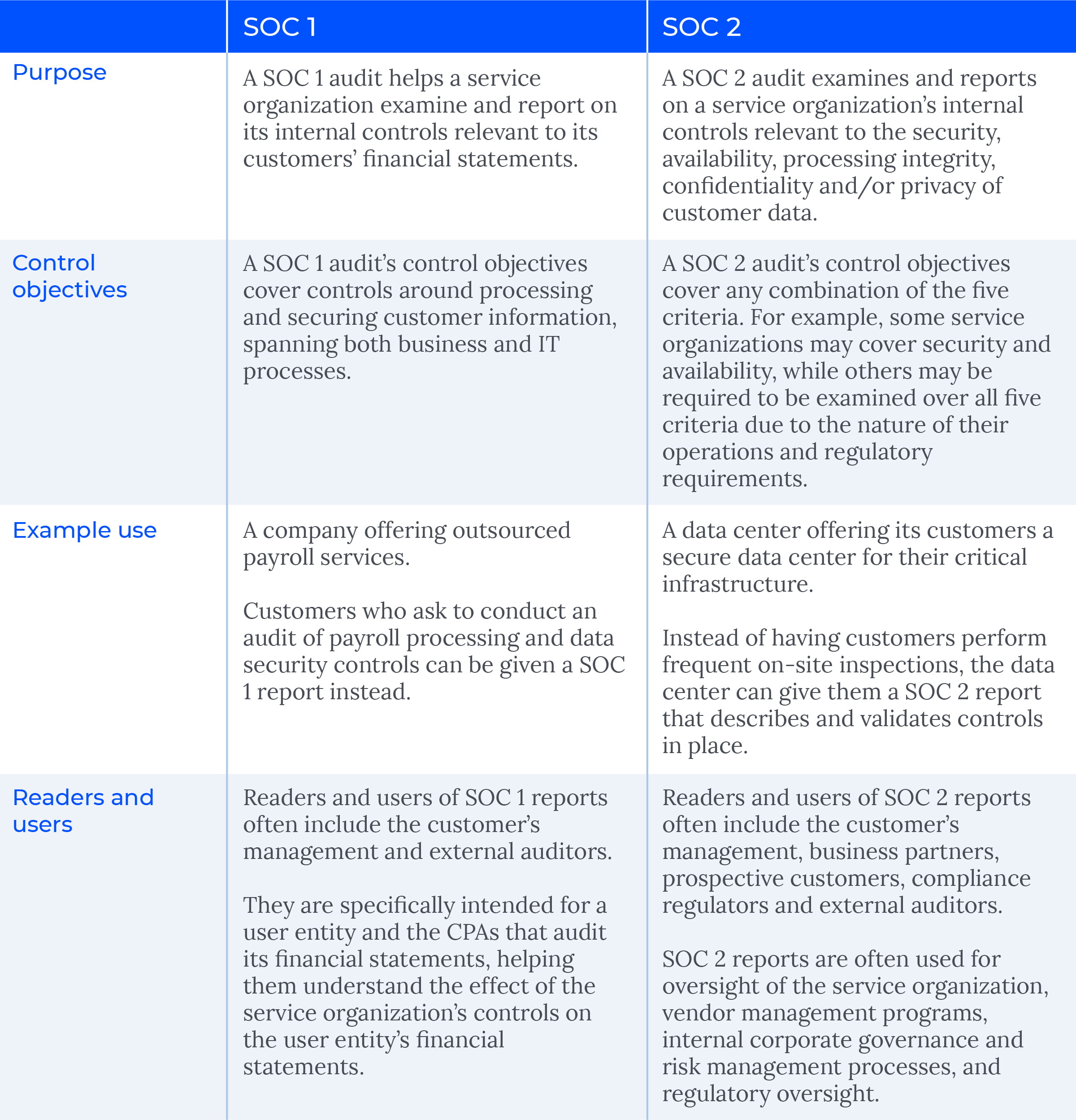

Soc 1 Vs Soc 2 What S The Difference Wipfli

Monthly Productivity Report Template 1 Templates Example Templates Example In 2020 Report Template Project Status Report Statement Template

Template Net 25 Incident Report Templates In Word Free Premium Templates 39e2be57 Resumesample Resumefor

Presentence Investigation Report Template 2 Templates Example Templates Example In 2020 Report Template Templates Investigations

Test Closure Report Template 5 Templates Example Templates Example Report Template Templates Professional Templates

Hurt Feelings Report Template 11 Professional Templates Incident Report Report Template Incident Report Form

Monthly Productivity Report Template 5 Templates Example Templates Example Di 2020